Your Retirement, Made Simple

Compare pension plans, calculate your retirement needs, and secure your future with ease

3 Steps to Secure your Future

Know How Much you Need to Retire Rich & Stress-free

Pension Calculator

You need monthly income of

₹0/month

at the age of 60

Based on 5% Inflation. See how?

To get a corpus of

₹6.70Cr

in 20 years @15% CAGR

Which gives you

Income for life

/month for household expenses

from ₹3.70Cr invested in annuity @7%

Any other big expenses to plan for in retirement?

Plan for Big Events

Your retirement isn't just about daily expenses. Factor in life's major milestones to ensure you're fully prepared.

On retirement, you'll need

₹3.00Cr

for your big events.

To get a corpus of

₹6.70Cr

in 20 years @15% CAGR

Which gives you

Income for life

/month for household expenses

from ₹3.70Cr invested in annuity @7%

Lumpsum payout

₹1.94 Cr

for your big events

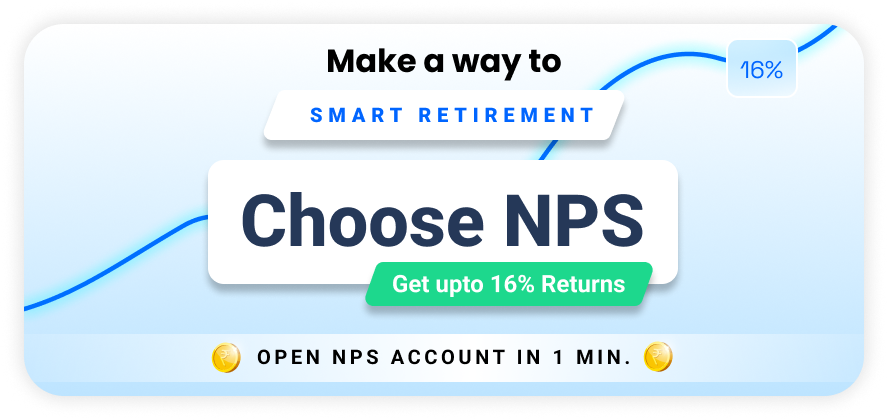

NPS – “The Smarter Way to Retire”

The National Pension System (NPS) is a market-linked, voluntary and defined contribution pension scheme in India regulated by the PFRDA which helps subscribers plan and save for their retirement. NPS is an EEE (exempt-exempt-exempt) scheme under which significant tax benefits are applicable in both investment & withdrawal phase.

High returns

Upto 16%*Historically delivered upto 16%* , outperforming most traditional pension products

(source: NPS trust for Tier I equity scheme)

Triple tax benefit on contributions

Save up to ₹2.7 L per annumSave taxes under Section 80CCD (1), 80CCD (1B) & 80CCD (2)

Government backed

PFRDA regulatedRegulated and secured by PFRDA, ensuring transparency and safety

Tax free withdrawal + Assured pension at retirement

80% lump sum | 60% tax-freeWithdraw up to 80% of your NPS corpus at retirement, with 60% completely tax-free, and use the rest to receive a guaranteed lifelong pension.

Market-linked growth

Equity & debt mixGrow your wealth with professional fund management across equities, corporate bonds & government securities

Lowest-cost retirement product

Charges <0.3% in IndiaNPS has one of the lowest charges across pension options available in India (<0.3%)

Shri Sivasubramanian Ramann

Chairperson of the Pension Fund Regulatory and Development Authority (PFRDA)

How to start NPS

via Pensionbazaar

Invest in NPS

In less than a minute

STEP 01

Basic details & KYC

Share a few essentials to get your journey started

STEP 02

Compare & choose your plan

Explore options and pick a plan that suits your goals

STEP 03

Finalise & review your detail

One last check before you invest

STEP 04

Invest & let your money grow

Start now. Retire stress-free.

A Quick Look at the Popular Retirement Planning Options

Annualised

Returns

Tax Exemption on Investment

Taxation on Maturity

Contribution Limit (Per Financial Year)

Flexible Investment options

Exempt

(u/s 80 CCD)

Partially taxable

(Upto 60%

corpus tax free)

No Limit

![]() Yes

Yes

7.1%

Exempt

(upto 1.5 L u/s 80C)

Tax free

1.5 L

(in a Financial

Year)

![]() No

No

8.2%

Exempt

(upto 1.5 L u/s 80C)

Partially taxable

(upto 50K can be

exempted)

30 L

(Lifetime)

![]() No

No

Exempt

(upto 1.5 L u/s 80C)

Partially taxable

(exempt if annual premium is less than 2.5L)

No Limit

![]() Yes

Yes

7.4%

Exempt

(upto 1.5 L u/s 80C)

Taxable

9 L

(Lifetime)

![]() No

No

10%–12%

Taxable

(select MF exempt)

Taxable

No Limit

![]() Yes

Yes

6%-7%

Taxable

Taxable

No Limit

![]() No

No

Taxable

Taxable

No Limit

![]() Yes

Yes

Let's Understand the Tax Exemptions

The national pension system can offer lakhs in tax savings.

Let's understand tax the exemptions you can avail on NPS contributions!

Old Tax Regime

-

₹1.5 L –

Your contribution under section 80 CCD (1)*

₹1.5 L –

Your contribution under section 80 CCD (1)*

-

50 K –

Additional under section 80 CCD(1b)

-

14%^ of basic salary -

Additional under section 80 CCD(2) -

Employer contribution to NPS from your CTC

* Subject to max ₹1.5L under 80C

^ 14%

for government, 10% for private sector employees

New Tax Regime

-

14% of basic salary –

Additional under section 80 CCD(2) – Employer

contribution to NPS from your CTC

Self Employed

-

Upto 20% of gross total income, subject to maximum of ₹1.5L under section 80 C

Types of NPS Account

01 Tier I Account

The primary, tax-benefit retirement account under NPS with low minimum yearly contributions

-

Who can open:

All eligible subscribers (Residents, NRIs, OCIs)

-

Minimum contribution:

- • ₹500 at account opening

- • ₹1,000 per financial year (to keep account active)

-

Withdrawals:

- • You can make up to four partial withdrawals before retirement

- • Minimum 15 years or until age 60, whichever is earlier

-

Tax Benefits:

• Tax benefit on investments

- • ₹1.5 lakh u/s 80CCD(1) (within the overall limit)

- • Additional ₹50,000 u/s 80CCD(1B)

- • Upto 14% of basic salary (over and above) u/s 80CCD(2) - Employer Contribution to NPS from your salary

• Tax Benefit on Maturity Amount:- • At retirement, you can withdraw up to 80% as a lump sum and use the remaining 20% to buy an annuity.

- • Up to 60% of the corpus can be withdrawn tax-free as lump sum

- • Minimum 20% must be invested in an annuity the investment is tax-free, while annuity income is taxable

Best for: Investors who want to use NPS for retirement planning

Best for: Investors who want to use NPS for retirement planning

02 Tier II Account

A voluntary, flexible savings account under NPS with easy withdrawals.

-

Who can open:

Only those who already have a Tier I account (Not available to NRIs/OCIs)

-

Minimum contribution:

₹1,000 at account opening, ₹250 per transaction

-

Withdrawals:

Anytime, no restrictions

-

Tax Benefits:

• Tax benefit on investments : Nil

• Maturity amount is taxable

Best for: Investors who want to use NPS for short/medium-term savings

with low charges.

Investment Choices in NPS

01 Auto Choice (Life-Cycle Fund)

Is Hands-Free Approach, ideal for beginners who don't want to actively manage allocations. The mix of equity and debt adjusts automatically as you grow older.

-

Life Cycle 25 – Low Equity exposure starts at 25% till age 35 and gradually reduces to 5% after age 55

-

Life Cycle 50 – Moderate Equity exposure starts at 50% till age 35 and gradually reduces to 10% after age 5

-

Life Cycle 75 – High Equity exposure starts at 75% till age 35 and gradually reduces to 15% after age 55

-

Life Cycle – Aggressive Equity exposure starts at 50% till age 45 and gradually reduces to 35% after age 55

Best for: First-time investors who prefer a "set-and-forget" approach

02 Active Choice - DIY Allocation

If you want to design your own portfolio, you can split contributions across these asset classes (subject to limits):

-

Equity (E): Invested in listed shares (max 75% till age 50; reduces after that). Higher risk, higher return potential

-

Corporate Bonds (C): Debt issued by corporates. Moderate risk, stable income

-

Government Securities (G): Sovereign bonds. Lowest risk, steady returns

-

Alternative Assets (A): REITs, InvITs, etc. (Max 5%). For diversification

Best for: Experienced investors who want control and have risk appetite

03New Pension Schemes

-

Choose high-growth options with equity exposure of up to 100%

-

Flexible exit after 15 years or on reaching age 60 whichever is earlier

-

Invest across multiple pension schemes under one NPS account

-

Pension Fund Managers can offer customised schemes for different investor groups with varying risk levels

Pension Fund Managers (PFMs)

Your contributions are managed by licensed Pension Fund Managers (PFMs). You can choose one from the list and even switch later.

Current PFMs include:

Historical Returns

Past performance of different asset classes in NPS.

Note: Past performance does not guarantee future returns.

Group Brands

Edit

Edit