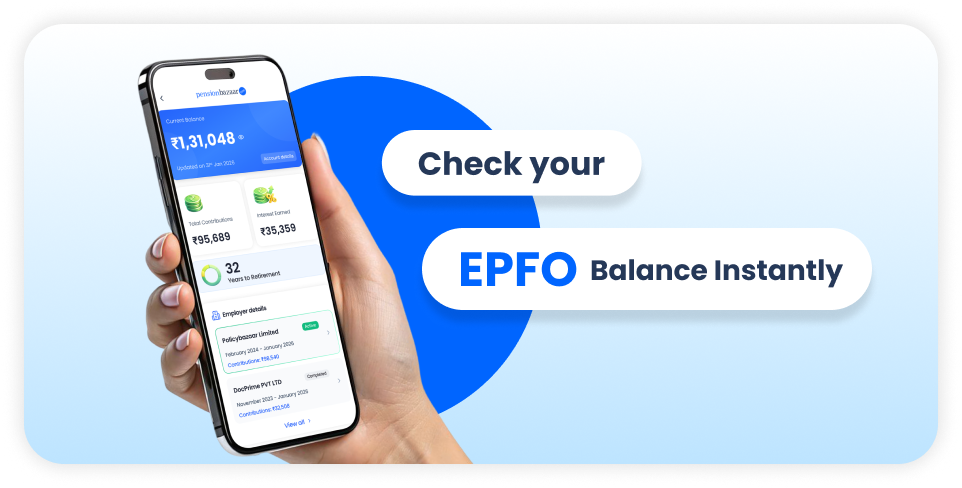

Employee Provident Fund

The Employee Provident Fund (EPF) is a statutory savings scheme for salaried employees in India, managed by the EPFO. It acts as a foundational retirement tool where both employees and employers contribute a fixed monthly percentage of the basic salary. The accumulated corpus grows through annually declared compound interest, providing long-term financial stability.

Public Provident Fund

The Public Provident Fund (PPF) is a secure, government-backed savings avenue designed to encourage long-term capital accumulation among all Indian citizens. Featuring a fixed fifteen-year tenure and legally guaranteed returns, it provides a stable investment option. The interest earned and the final maturity amount are completely tax-exempt under sovereign statutory provisions.

Pension And Other Plans

Pension Plans encompasses a diverse range of institutional pension frameworks, superannuation models, and government-backed social security programmes. These initiatives are designed to cater to different segments of the workforce, offering structured financial relief through fixed annuities, monthly stipends, or senior citizen benefits to ensure continuous financial protection during post-work lifespans.

Retirement Planning

Retirement planning is the strategic process of evaluating future living expenses, inflation trends, and life expectancy to achieve long-term financial autonomy. Retirement Planning discipline involves calculating required corpus sizes, managing active asset allocations, and establishing structured withdrawal strategies, ensuring that individuals accumulate sufficient wealth to maintain their desired lifestyle after leaving active employment.

Annuity

An annuity is a specialised financial contract that converts a lump-sum retirement corpus into a guaranteed, regular stream of income. Functioning as the core mechanism of the retirement decumulation phase, annuity mitigates the risk of individuals outliving their capital by delivering lifetime monthly or annual payouts through empanelled life insurance service providers.

Mutual Funds

Mutual funds are pooled investment vehicles managed by professional asset management companies to invest in diversified portfolios of equities, corporate debt, and government securities. Operating through systematic investment plans or lump-sum allocations, these market-linked instruments enable everyday investors to benefit from compound growth, capital appreciation, and risk optimization over extended time horizons.

Corporate NPS

Corporate National Pension System (Corporate NPS) is an employer-sponsored retirement savings scheme that enables employees to build a retirement corpus while enjoying additional tax benefits. It complements salary benefits and encourages disciplined, long-term retirement planning.

NPS Vatsalya

NPS Vatsalya is a government-backed pension scheme for minors that allows parents or guardians to start investing early for their child's financial future. The account can continue seamlessly into a regular NPS account once the child reaches adulthood.

Atal Pension Yojana

Atal Pension Yojana (APY) is a government-backed pension scheme aimed at workers in the unorganised sector. It helps subscribers build a retirement corpus and provides a guaranteed monthly pension after the age of 60, subject to scheme conditions.

Edit

Edit